Delta Hedging

To show how Delta Hedging can be done with MesoSim, let’s consider a structure consisting of two legs (separate option contracts):

- 1 Call Option:

sold at around 160 DTE with the Strike closest to 10 delta. This leg will be referred to asshort_call. - 1 Put Option:

sold at the same expiration as the call with the Strike selected to bring the whole structure (Short Call and Short Put together) closest to 0 delta. Practically that delta will also be around 10, but we’ve chosen to do this calculation dynamically. This leg will be referred to asshort_put.

"Structure": {

"Name": "ShortStrangle",

"Expirations": [

{

"Name": "160dte",

"DTE": "160",

"Min": 140,

"Max": 190

}

],

"Legs": [

{

"Name": "short_call",

"Qty": "-1",

"ExpirationName": "160dte",

"StrikeSelector": {

"Min": 5,

"Max": 15,

"Delta": "10"

},

"OptionType": "Call"

},

{

"Name": "short_put",

"Qty": "-1",

"ExpirationName": "160dte",

"StrikeSelector": {

"Min": 5,

"Max": 15,

"Delta": "leg_short_call_delta * -1"

},

"OptionType": "Put"

}

]

}

The delta selector for the short_put leg uses the previously defined short_call leg’s delta.

The resulting structure’s overall delta will be around 0.

The above approach is easy to understand and works, but there is a better, more scalable way of doing it.

To illustrate, let’s consider a three-legged structure, a Broken Wing Butterfly:

"Legs": [

{

"Name": "upper_long",

"Qty": "1",

"ExpirationName": "160dte",

"StrikeSelector": {

"Delta": "40"

},

"OptionType": "Put"

},

{

"Name": "short",

"Qty": "-2",

"ExpirationName": "160dte",

"StrikeSelector": {

"Delta": "30"

},

"OptionType": "Put"

},

{

"Name": "lower_long",

"Qty": "1",

"ExpirationName": "160dte",

"StrikeSelector": {

"Delta": "pos_delta"

},

"OptionType": "Put"

}]

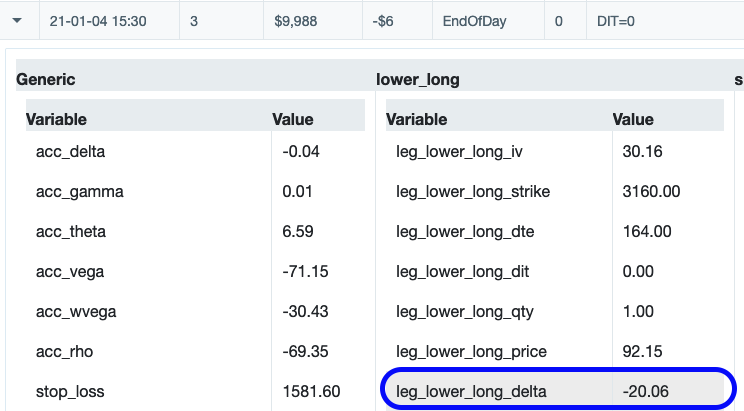

In the above example, the last leg’s (lower_long) delta is specified using a statement that is calculated based on the overall position delta so far.

At the time of the statement evaluation, two legs are already considered, and pos_delta represents their sum:

pos_delta = [ leg_upper_long_delta ] + [ leg_short_delta ]

= [1 x (-40)] + [-2 x (-30)]

= -40 + 60

= 20

If we take this delta value (which should be around: (2*30)-40=20) and choose the last (lower_long) leg using this delta value then we will end up at a delta neutral position at initiation: